All Categories

Featured

Table of Contents

If you're someone with a low resistance for market fluctuations, this insight could be indispensable - IUL investment. Among the vital facets of any type of insurance plan is its price. IUL plans often include different fees and charges that can influence their general worth. A monetary consultant can break down these costs and assist you weigh them against various other low-cost financial investment choices.

Pay particular focus to the policy's features which will be crucial depending upon how you desire to make use of the plan. Talk to an independent life insurance policy agent that can help you select the best indexed global life plan for your needs.

Evaluation the plan carefully. Now that we've covered the advantages of IUL, it's essential to comprehend how it contrasts to various other life insurance policy policies available in the market.

By recognizing the similarities and distinctions in between these policies, you can make a much more enlightened choice concerning which sort of life insurance policy is ideal fit for your needs and financial objectives. We'll begin by comparing index global life with term life insurance policy, which is frequently considered one of the most simple and cost effective kind of life insurance policy.

What happens if I don’t have Iul Policyholders?

While IUL may supply greater prospective returns due to its indexed cash value growth device, it also comes with higher costs compared to term life insurance coverage. Both IUL and whole life insurance coverage are sorts of permanent life insurance policy plans that offer death advantage protection and cash value development possibilities (IUL financial security). There are some essential differences between these 2 kinds of policies that are vital to take into consideration when deciding which one is ideal for you.

When taking into consideration IUL vs. all various other types of life insurance coverage, it's important to consider the benefits and drawbacks of each plan kind and seek advice from with a skilled life insurance agent or financial advisor to identify the ideal option for your distinct requirements and monetary goals. While IUL uses several advantages, it's likewise essential to be aware of the risks and considerations related to this sort of life insurance coverage policy.

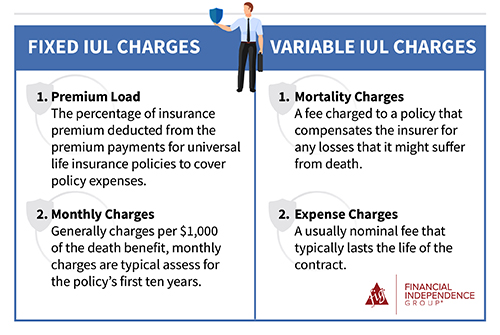

Let's dig deeper into each of these risks. Among the main issues when taking into consideration an IUL policy is the various expenses and costs related to the plan. These can consist of the expense of insurance policy, plan charges, surrender charges and any type of added motorcyclist prices sustained if you include added benefits to the policy.

Some might offer extra competitive rates on protection. Examine the financial investment options available. You want an IUL plan with a series of index fund options to satisfy your demands. Make certain the life insurance provider straightens with your individual financial goals, needs, and threat tolerance. An IUL policy ought to fit your certain circumstance.

What is included in Iul Growth Strategy coverage?

Indexed universal life insurance policy can provide a variety of benefits for insurance holders, consisting of adaptable premium settlements and the prospective to make higher returns. The returns are restricted by caps on gains, and there are no warranties on the market performance. All in all, IUL plans provide a number of prospective advantages, however it is important to recognize their threats.

Life is not worth it for most people. For those looking for foreseeable lasting savings and ensured death advantages, entire life might be the better option.

Why is Indexed Universal Life Growth Strategy important?

The benefits of an Indexed Universal Life (IUL) plan consist of prospective higher returns, no drawback risk from market movements, defense, adaptable settlements, no age demand, tax-free survivor benefit, and car loan schedule. An IUL policy is long-term and provides money worth growth through an equity index account. Universal life insurance began in 1979 in the United States of America.

By the end of 1983, all significant American life insurance providers supplied universal life insurance policy. In 1997, the life insurance provider, Transamerica, presented indexed universal life insurance coverage which offered insurance holders the capability to connect policy development with international securities market returns. Today, global life, or UL as it is likewise understood can be found in a variety of various kinds and is a huge part of the life insurance policy market.

The information supplied in this post is for educational and informative functions just and must not be interpreted as financial or financial investment suggestions. While the author has knowledge in the subject, viewers are encouraged to consult with a qualified economic consultant before making any investment choices or acquiring any life insurance policy products.

Why do I need Iul Insurance?

You may not have actually believed a lot about exactly how you desire to invest your retirement years, though you possibly understand that you don't want to run out of cash and you 'd such as to maintain your present lifestyle. [video: Text appears next to the business man speaking to the camera that reads "company pension", "social security" and "savings". IUL death benefit.] < map wp-tag-video: Text shows up alongside the organization male talking with the video camera that reads "business pension plan", "social security" and "savings"./ wp-end-tag > In the past, people relied on three primary income sources in their retired life: a firm pension, Social Safety and whatever they would certainly handled to conserve

Less companies are using typical pension plan plans. Also if advantages have not been reduced by the time you retire, Social Safety and security alone was never planned to be enough to pay for the way of living you desire and should have.

Prior to dedicating to indexed universal life insurance policy, below are some advantages and disadvantages to take into consideration. If you select a great indexed universal life insurance policy strategy, you may see your cash value expand in worth. This is helpful since you may be able to access this cash before the plan runs out.

What is the difference between Indexed Universal Life Calculator and other options?

Given that indexed universal life insurance policy requires a specific level of danger, insurance business tend to keep 6. This type of plan also provides.

If the selected index does not perform well, your money worth's growth will certainly be affected. Commonly, the insurance policy company has a beneficial interest in executing far better than the index11. There is generally an assured minimum passion price, so your plan's growth will not drop below a certain percentage12. These are all factors to be taken into consideration when choosing the ideal kind of life insurance policy for you.

Given that this kind of policy is a lot more complex and has an investment element, it can usually come with greater premiums than other plans like entire life or term life insurance coverage. If you don't believe indexed global life insurance coverage is appropriate for you, right here are some alternatives to think about: Term life insurance is a short-lived plan that typically provides insurance coverage for 10 to 30 years

{kind=link}

Latest Posts

What Is Iu L

Index Universal Life Insurance Reddit

Indexed Universal Life Insurance Good Or Bad